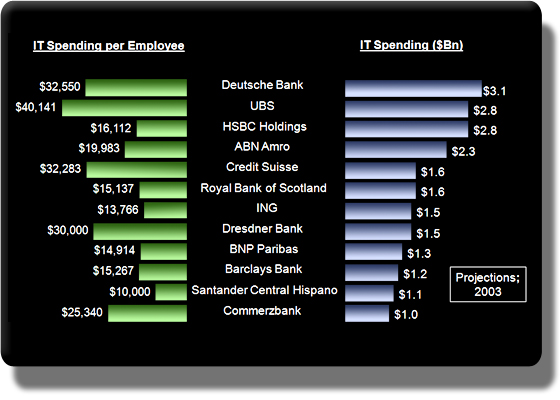

Leading European Banks: Projected IT Spending, 2003P

A combination of high industry concentration in the national markets,

a vendor community that is underdeveloped relative to the US market, and

a tendency for larger institutions to undertake (costly) in-house development,

help explain the levels of technology spending among leading European

banks. Spending projections shown

represent our expectations for global technology investment by the institution

during 2003. Technology spending per head is lower for banks with more

of a retail focus and higher for those with more substantial capital markets

units.

Source: Nechtain